In February, International equities once again outperformed and returned +4.6%. This compared to the US where the S&P 500 declined -0.8%. Surprisingly, this month’s significant outperformance of International stocks came despite strength in the US Dollar. Large Cap Tech names underperformed in February while small-cap stocks, cyclical and value-oriented sectors outperformed. This nascent market rotation may be signaling a broadening out of underlying economic health in the U.S. economy. A continuation of this trend would be a very healthy resolution to the high stock market concentration we have previously written about.

The U.S. 10-year Treasury yield fell sharply in February and ended the month at 3.94%. The initial Q4 2025 measure of GDP growth came in at +1.4%—less than half what most economists were expecting. The record long government shutdown may partially explain the low number. Weak retail sales data from late 2025 was also a contributing factor. However, the Fed’s GDPNow estimate for Q1 2026 currently projects a rebound in growth to +3%. The Supreme Court ruled that President Trump exceeded his tariff authority and ordered a roll back of tariffs. Oil prices began to rise in anticipation of US military action in Iran. Oil prices may put pressure on inflation, which could in turn pressure interest rates and stocks.

| Index | February | YTD | Index | February | YTD |

|---|---|---|---|---|---|

| S&P 500 (Total Return) | -0.76% | +0.68% | MSCI All Country World (Net) | +1.29% | +4.29% |

| MSCI EAFE (Net) | +4.63% | +10.09% | Bloomberg Barclays US Agg | +1.64% | +1.75% |

| MSCI Emerging Markets (Net) | +5.41% | +14.69 | 60/40 Blend* | +1.44% | +3.28% |

* 60% All Country World Index / 40% Bloomberg Barclays US Aggregate Bond Index

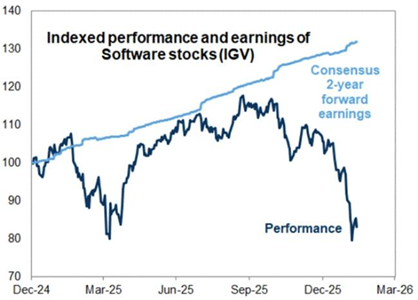

The software sector has experienced weak performance to start the year which is noteworthy because over the prior three years it has significantly contributed to technology, which in turn has driven strong U.S. equity market returns. For example IGV, an ETF representing the broad US public software sector, is down -22% through the end of February. As a starting point, we must first consider software’s performance over the past few years. Following a difficult 2022 in which the sector declined -35%, software companies’ performance recovered in 2023 and went on to generate a 125% cumulative return versus the S&P 500’s return of 81% through Q3 2025. A contributing factor to this subsequent outperformance was multiple expansion, which left IGV trading at an expensive 40x forward earnings multiple. Following recent negative stock performance and earnings reports, the software sector now trades at approximately 23x forward earnings, which is its lowest valuation level over the past ten years.

Software companies have historically traded at a 50-70% earnings valuation premium to the S&P 500 because of their high growth and profitable business models but today trade at roughly the same valuation as the broader market. A significant portion of software’s poor performance has been due to multiple compression rather than earnings declines. So why is the software sector experiencing valuation compression?

One explanation for software’s multiple compression has been the advancement of Artificial Intelligence’s capabilities. Two risks of Artificial Intelligence for software companies are concerns that AI can rapidly write code that lowers legacy software’s competitive advantages, and if AI leads to less employee hiring among companies, the per-user revenue models of some software companies will be disrupted. The market may be anticipating that software companies’ revenue growth will be slower, they will be less profitable in the future, or some combination of both. This doesn’t necessarily mean that software companies will stop growing, but they might grow at a slower rate than historical levels.

While Artificial Intelligence will likely reshape how these companies operate, it is important to remember that not all software companies are equally at risk. Businesses that provide mission critical services to corporate end-clients and maintain access to propriety data may be insulated, as they support complex workflows. These companies are well-positioned to benefit from AI by embedding it into their existing workflows which expands the capabilities that customers are willing to pay for. Conversely, software companies offering generic or single point solutions (e.g., basic back-office automation)—will likely face headwinds as AI can replicate many of their services.

Many software companies have experience navigating shifts in revenue models. A key example of this was in the early 2010s when many vendors shifted from “license and maintenance” models to “subscription-based pricing models” following the advent of cloud-based software. The transition was initially viewed as complex and there was uncertainty regarding customer value perception under the new subscription model. In this current transition, businesses may develop hybrid pricing models that blend traditional per-user fees with variable AI usage fees. This could help offset the impact of fewer subscriptions being needed by physical users and capture the potential upside from AI agents.

The concerns regarding AI have not shown up in the fundamental earnings of publicly traded software companies yet. Similarly, Caprock’s private credit managers have some exposure to software in their highly diversified loan portfolios and note that software companies have performed well. Specifically, the middle market software companies they lend to achieved double-digit EBITDA growth in 2025 and are expected to achieve similar growth in 2026, supporting strong fundamentals.

Readers will notice in the chart below that in March 2025 software companies were under significant pressure, but share prices eventually rebounded because the concerns did not ultimately show up in earnings. Software stocks were beginning to recover from the 2025 tariff shock until the recent developments in AI created new concern. When stocks drastically dislocate from fundamentals it is typically during periods of peak market uncertainty regarding a new and potentially negative development, resulting in multiple compression. The market is actively debating the true value of software companies, which will eventually be validated by operating performance.

During this period of price discovery, there may be a widening gap between public market sentiment and private operating reality. Private companies are more nimble and able to create value faster through more rapid AI product development and transformation. The public markets will likely wait for clearer AI revenue and efficiency data points, which will take time as financial metrics lag implementation. We expect there to be winners and losers in the software space, but do not believe the entire sector is at risk of disruption.

What we’re reading:

Below we share a glimpse into the books currently capturing the interest of the Caprock team – highlighting the diverse tastes and curiosity that drive our team.

Ashley Laney, a client associate on our Advisory team, has recently finished and is currently reading the following books:

- Moving Mountains: Creating the Nurse Practitioner and Rural EMS by Marie and John Osborn: This inspiring story explores resilience, purpose, and the power of perseverance in the face of overwhelming challenges. Marie and John Osborn chronicle their journey through personal adversity with honesty and humility, offering a reminder that meaningful progress is often built through small, deliberate steps rather than grand gestures. What makes Moving Mountains especially compelling is its balance of emotional depth and practical wisdom. It doesn’t shy away from hardship but instead reframes struggle as a catalyst for growth and connection. The book serves as a thoughtful reflection on leadership, partnership, and the quiet strength required to keep moving forward when the path ahead feels uncertain.

- The Midnight Library by Matt Haig: A reflective, imaginative novel that explores the infinite possibilities of life and the quiet weight of regret. Through the story of Nora Seed, who finds herself in a library between life and death, where each book represents a different version of the life she could have lived. Haig examines the choices that shape our identities and the tendency to measure our lives against imagined alternatives. The novel blends philosophy and storytelling in an accessible, relatable way, encouraging readers to reconsider how they define fulfillment and success. Ultimately, The Midnight Library is a hopeful meditation on perspective, reminding us that meaning is often found not in perfection, but in embracing the life we are already living.

- Blink by Malcolm Gladwell (currently reading): In Blink, Malcolm Gladwell explores the power and pitfalls of rapid decision-making, examining how our brains make split-second judgments before we’re even consciously aware of them. Through a mix of psychology, neuroscience, and compelling real-world examples, Gladwell challenges the assumption that careful analysis always leads to better outcomes. The book raises thoughtful questions about intuition, bias, and expertise, encouraging readers to reflect on when instincts can be trusted and when they can mislead us. So far, Blink has been an engaging and thought-provoking read, offering valuable insights into how we process information and make decisions in fast-paced environments.

This communication is not an offer or solicitation with respect to the purchase or sale of any security and is for informational purposes only. Information contained herein has been derived from sources believed to be reliable, but Caprock makes no representations as to its accuracy or completeness. Investment in securities involves the risk of loss. Past performance is no guarantee of future returns.