Executive Summary

After selling his homebuilding business to a national buyer, James found himself at an inflection point. The transaction created significant capital. However, most of his investments outside of the business were tied to real estate holdings. This exposed a new challenge of how to broaden his mix of assets while keeping enough liquidity for future development projects.

James, still in his professional prime, was not stepping away from investing in business. He wanted flexibility to pursue new opportunities while ensuring that the wealth he had created could support his family, manage risk, and advance his philanthropic efforts.

His balance sheet was fragmented across multiple trusts, entities, and accounts. Maintaining and organizing all the assets and structures was becoming cumbersome and lacked a cohesive whole. He had established a foundation actively engaged in change-making efforts. However, gifting was inconsistent, administrative responsibilities were unclear, and decision-making had become slower at precisely the moment clarity mattered most.

At a Glance

-

Liquidity event from a large company sale

-

Ongoing development ventures

-

Concentrated real estate investment assets

-

Multiple trusts and entities

-

Married with three adult children

-

Active family foundation

Goals and Objectives

James faced several interconnected priorities:

- Maintaining liquidity for future development projects without disrupting existing long-term investments

- Reducing concentration risk while remaining aligned with his comfort around real assets

- Establishing clearer governance as his three adult children began to engage with the family’s wealth

- Integrating philanthropy into a broader legacy plan rather than treating it as a standalone activity

He required an integrated strategy that connected all these priorities.

Caprock’s Approach

Caprock took the lead, coordinating with his existing tax, legal and investment brokers to shift his balance sheet from a single-industry concentration to a diversified, multi-asset strategy while meeting long-term family and giving goals efficiently.

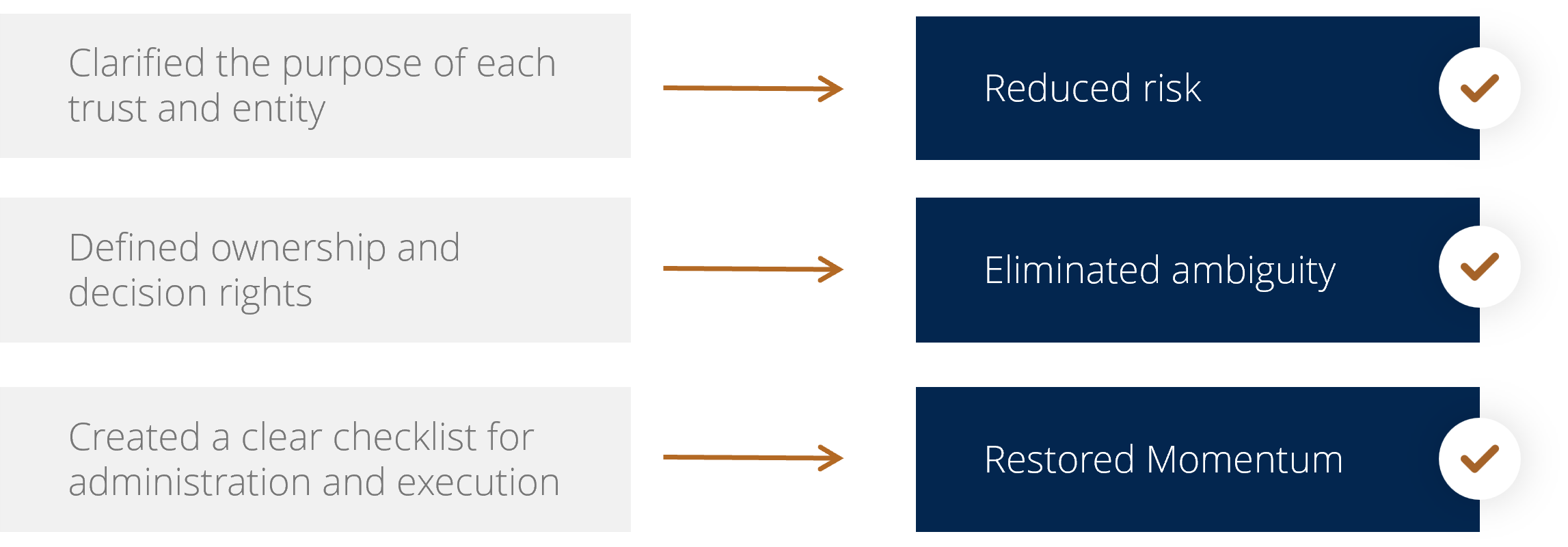

1. Caprock established a unified capital framework.

When James sold his business, he already had a network of trusts, entities and accounts. What was missing was a single plan that connected them and could adjust to changing needs. Gifting and trust administration were inconsistent, increasing tax and estate risks and slowing decision-making.

Working alongside James’s legal and tax advisors, Caprock clarified the purpose of each trust and entity, defined ownership and decision rights, and created a clear checklist for administration and execution. This reduced risk, eliminated ambiguity, and restored momentum.

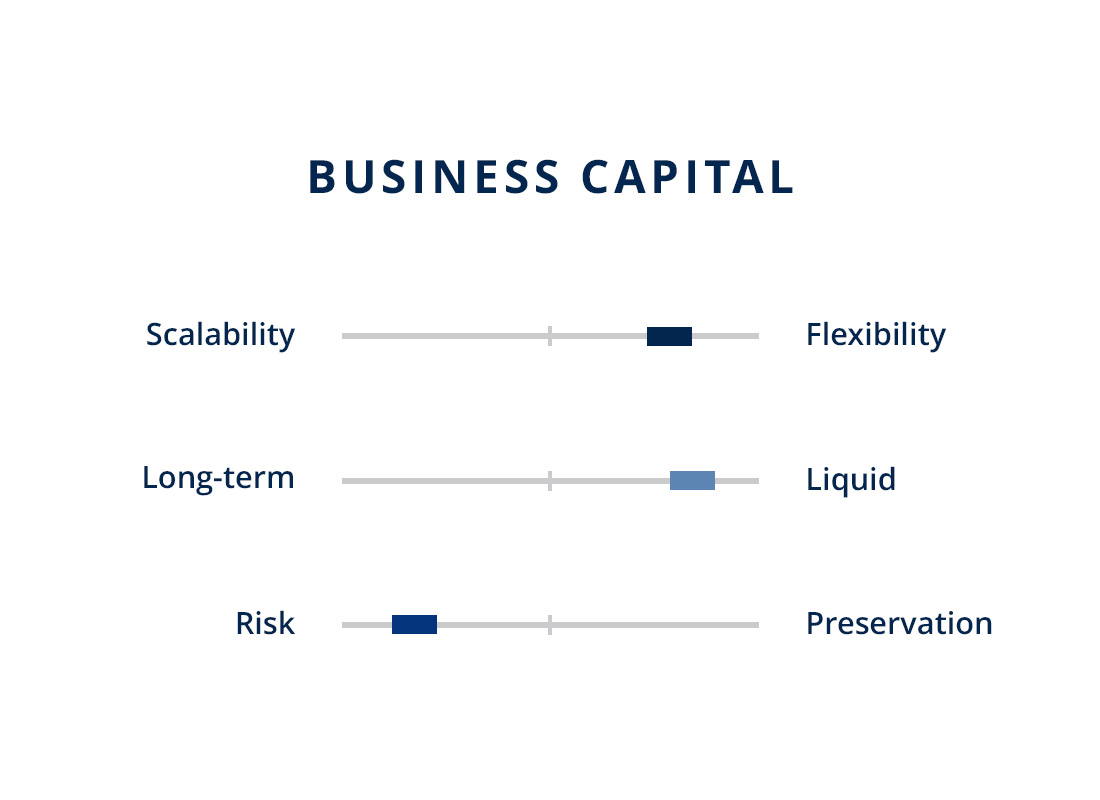

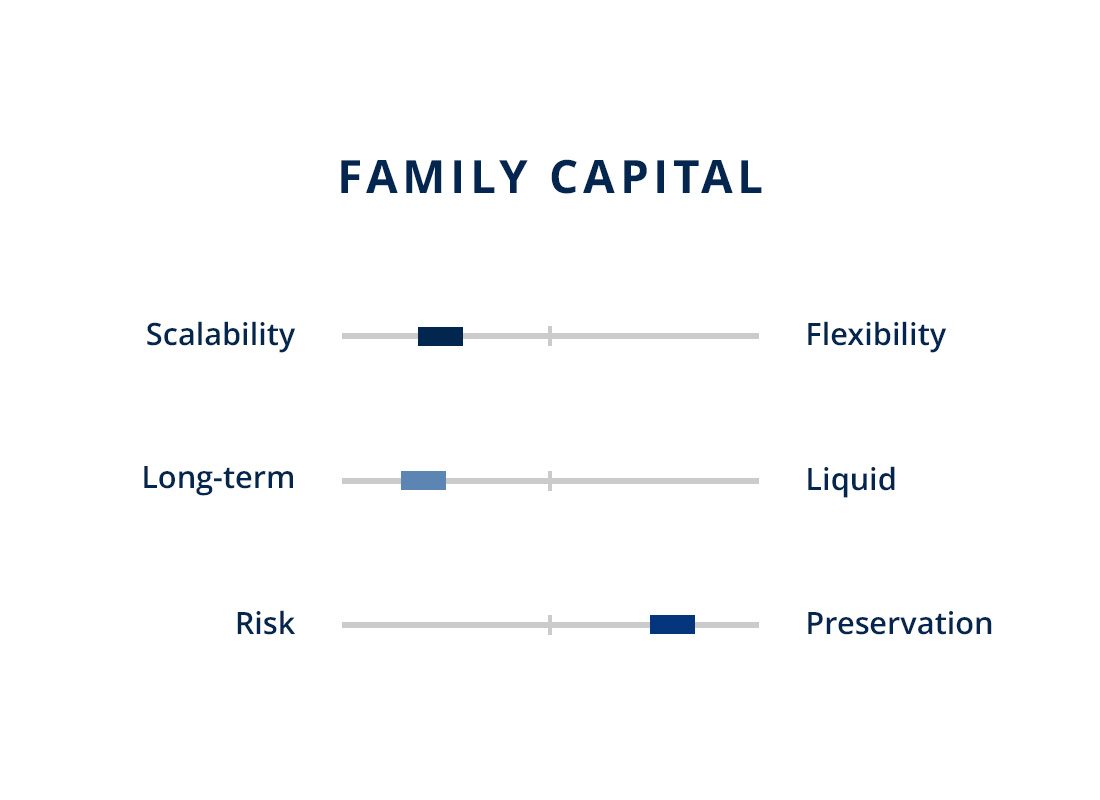

2. Caprock separated operating business exposure from long-term family capital.

Operating entities were reorganized to preserve flexibility for development activity, while family assets were positioned for stability and protection. Caprock separated the trusts and entities, making it easier to invest for stability rather than day-to-day business needs. This structure allowed James to pursue new opportunities without placing long-term wealth at unnecessary risk.

This process also surfaced governance issues that often get missed until there is a problem. In James’s case his business partner, named as a trustee, could no longer serve so an alternative was selected.

3. Caprock then redesigned liquidity with intention.

Rather than relying on liquidity within marketable securities, Caprock created tiered pools of capital that included near-term reserves and long-term investments.

Keeping everything in marketable securities can look liquid on paper, but it can force sales at the wrong time, so Caprock carved out true reserves for near-term project funding.

This made funding decisions more confident and prevented forced portfolio changes at inopportune times. Reports were organized to show where assets sat across entities and accounts and why each pool of capital was positioned the way it was.

4. Caprock evolved the portfolio and legacy plan in parallel

Given a large share of his net worth remained tied to concentrated real estate investments and an active development business, Caprock built a diversified portfolio. A diverse set of public and private investments were introduced gradually in alignment with James’s ongoing business ventures and risk tolerance. Caprock timed the investment steps to fit market conditions and the client’s need for cash.

Evolution of Investment Allocation: 2022, 2025

5. Integrate stewardship through gifting, education and philanthropy

As the children grew into adulthood, James and his wife wanted to bring them into the plan in a way that reinforced responsibility rather than entitlement. Caprock supported that through annual gifts, separate portfolios for each child and periodic meetings focused on long-term decision-making.

At the same time, the family foundation became a hands-on way for the next generation to become involved. Caprock incorporated the foundation into the family’s overall legacy plan, with clear roles, decision rights and a process to stay aligned on the values behind the work.

Fast Forward

Today, James operates with greater clarity and confidence. His capital is organized under a single strategy that supports both new ventures and long-term goals. Reporting is clearer, governance is stronger, and his children are engaged through education and responsibility.

What began as a liquidity event has become a structured framework for a family legacy and is designed to adapt as opportunities, markets, and generations evolve.

Contact Caprock for a personalized, no-obligation consultation.

*This case study is based on a current Caprock client, but the names have been changed to protect their identity and maintain confidentiality. The client was not compensated in any form. While every effort has been made to accurately portray the details of the case, certain elements may have been modified or excluded to further safeguard the privacy of the individual. This case study is intended for informational purposes only and should not be seen as a substitute for professional financial advice. The results and outcomes described in this document are specific to the individual client and may not be applicable to all situations. This case study is intended to provide general information about Caprock and is not a solicitation or offer to sell investment advisory services except in states where we are registered or where an exemption or exclusion from such registration exists.

©Caprock. The Caprock Group, LLC (“Caprock”) is an SEC Registered Investment Advisor. Registration with the SEC does not imply a certain level of skill or training.