Public equities are a powerful tool to help clients grow wealth while maintaining overall liquidity. While liquidity is advantageous for clients, it is important to understand the tax consequences and benefits associated with liquidity. Taxes on the increased value of a portfolio reduce overall portfolio performance when gains are ultimately realized. However, there are several tax-advantaged strategies with strong investment rationale that also reduce tax frictions. It is important to implement a thoughtful investment approach that continuously considers taxes and the timing of those payments.

The most popular and common tax-advantaged investment programs are traditional retirement plans such as 401(k)s, IRAs and Roth accounts. These accounts allow individuals to rebalance and adjust their portfolios without the common tax frictions associated with selling positions with embedded capital gains. An investor can adjust portfolios without tax implications, effectively deferring tax payments until retirement.

There are also less well-understood methods such as tax-loss harvesting, extension portfolios, options overlays, and 351 ETF conversions/exchange funds, which are tax-advantaged investment methods for high-net-worth and ultra-high-net-worth investors.

These vehicles require high-net-worth families, with the help of financial advisors, to actively manage their portfolios by integrating tax strategies with investment decisions. Taxes are a crucial factor to consider when deciding when to buy and sell equities or rebalance a broader investment portfolio.

For example, tax-loss harvesting is particularly important for entrepreneurs following liquidity events or during high-income years, when capital gains from a business sale, stock transactions, or investment distributions can significantly increase tax liability. By strategically realizing losses in other parts of a portfolio, entrepreneurs can offset gains, reduce tax drag, and improve after-tax compounding as they transition from concentrated business wealth to diversified assets. However, there are additional constraints and considerations such as transaction costs and market impact that could vary based on the individual circumstance.

For employees awarded significant equity for creating a disruptive product or platform, tax-aware methods such as staged sales, tax alpha capture, and exchange funds can help manage concentrated stock exposure while reducing the tax impact of realizing gains.

The ultimate goal should be compounding wealth at a higher rate of return through sound investment decisions and aligning the portfolio with client goals.

Tax-Aware Methods Available in Public Market Investing

Public markets are well-positioned for clients to deploy tax-advantaged investment methods because of their high liquidity and dynamic pricing. High-net-worth families should adopt a proactive approach that continuously integrates tax considerations rather than treating taxes as a year-end exercise. The implementation of tax-advantaged approaches depends on the asset classes held within an investment portfolio and each client’s unique tax circumstances

Public Equities

Portfolios with public equities may adopt a tax-loss harvesting strategy to offset stock gains, reduce ordinary income, or carry benefits forward. Charitable stock donations can also reduce portfolio concentration and generate tax deductions while allowing clients to achieve personal goals related to philanthropy.

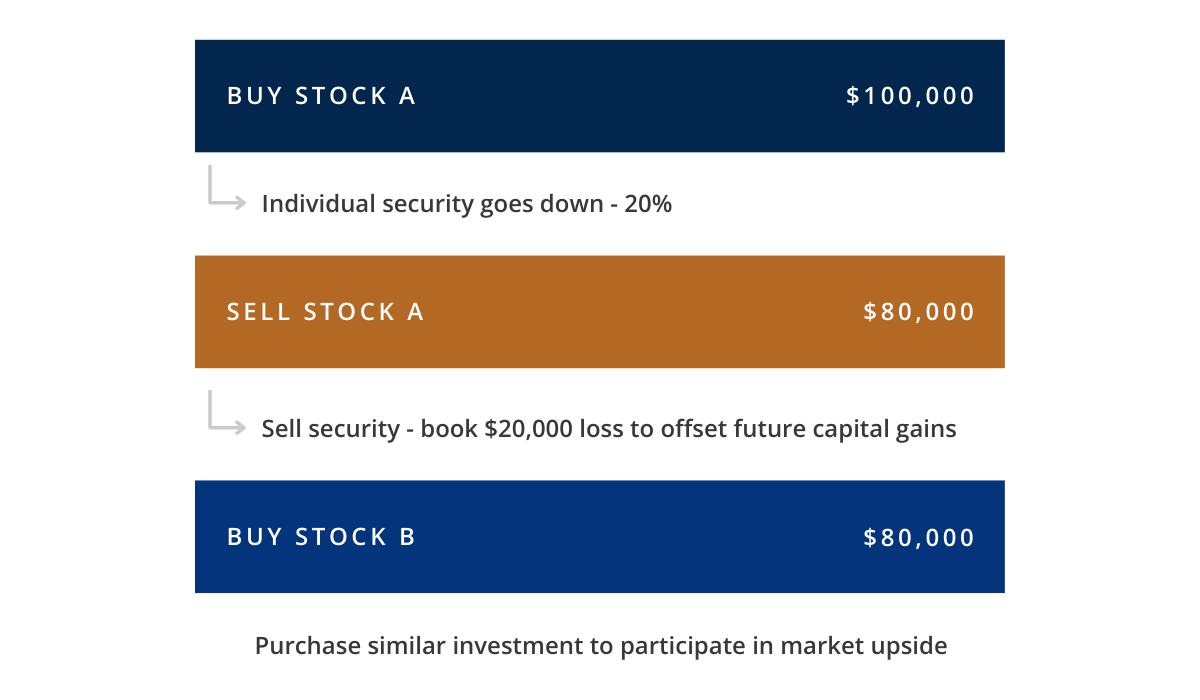

Tax-Aware Rebalancing Hypothetical Example

An investor spends $100,000 to purchase Stock A shares. The stock price drops 20%, which allows the investor to book a $20,000 loss. The investment is now worth $80,000. The investor uses the tax loss to finance the purchase of $80,000 worth of Stock B to participate in market upside.

Building an extension strategy around a core portfolio of equity holdings allows clients to preserve market exposure with additional benefits. High-net-worth families can use an investment manager’s skill to potentially improve investment performance while also realizing the latent tax benefits associated with the manager’s strategy. These managers invest in additional long positions expected to outperform, while also taking short positions that create tax losses as the market appreciates. 351 ETF Conversions enable investors to contribute equities with embedded gains to new investment strategies without realizing taxes. A client receives a new investment strategy packaged in the form of a liquid ETF.

Digital Assets

Portfolios with digital assets can offer after-tax compounding opportunities because of extreme price volatility. As of February 2026, traditional wash-sale rules do not apply to common digital assets such as Bitcoin and Ethereum. This means a sale and quick repurchase of the same asset still allows an investor to claim a short-term capital loss. There is substantial discussion about extending the wash-sale rule to cover digital assets and while no new rule has taken effect yet, future tax years could be different.

Options Overlays

Options overlays may be used to reduce investment risk while controlling the exit of a concentrated position. These methods generally seek to limit the downside risk of a large equity position and provide attractive investment characteristics such as income generation, smoothed volatility, and structured pathways towards exit. Although each option strategy is different and multiple methods may be used for concentrated stock, clients are typically capped in terms of their upside participation in stock. Use of this method often depend on an investors objectives and risk tolerance.

Fixed Income

Fixed-income assets can benefit from a focus on maximizing after-tax income instead of stated yields. Taxable or tax-exempt municipal bonds may be an option based on where an investor lives, their tax bracket and the type of bond. Tax-aware rebalancing can also be applied to bonds because they are sensitive to changes in interest rates and credit spreads.

Caprock broadly emphasizes the utilization of Separately Managed Accounts (SMAs), which can provide clients greater control and flexibility to utilize any of the above strategies in equity and fixed income portfolios.

Life‑Cycle of a Tax-Aware Public Markets Portfolio

Financial advisors can help clients develop a strategy for each stage of their portfolios. Every investor has unique circumstances, but there are some general stages.

Early Stage: In a recently funded portfolio, there are usually no large, embedded capital gains. Therefore, investors have the flexibility to capture tax losses without utilizing more complex methods. This is typically a good opportunity to review the portfolio and adjust without significant tax implications.

Mid Stage: Portfolios have some embedded capital gains, adjusting more likely to incur taxes. Investors may begin discussions with advisors on extension strategies. Investors with large private holdings anticipating liquidity events should prepare extension portfolios prior to the liquidity event if possible.

Late Stage: The portfolio has large, embedded capital gains, which may require more broad and intensive use of tax deferral methods. Extension methods, 351 ETF conversions, exchange funds, charitable giving, and complex estate planning may be used.

A Tax Strategy Glossary

Tax-loss harvesting is when investors recognize a loss by selling a stock that is lower than its purchase price. The resulting benefit allows high-net-worth families to offset embedded capital gains in other stocks that should be reduced. Clients can also use carryforwards to offset ordinary income or future capital gains. The cash proceeds from the initial stock sale can be used to purchase a security that shares similarities.

Tax alpha is the value created by the effective tax management of a portfolio allowing for greater compounding of returns going forward.

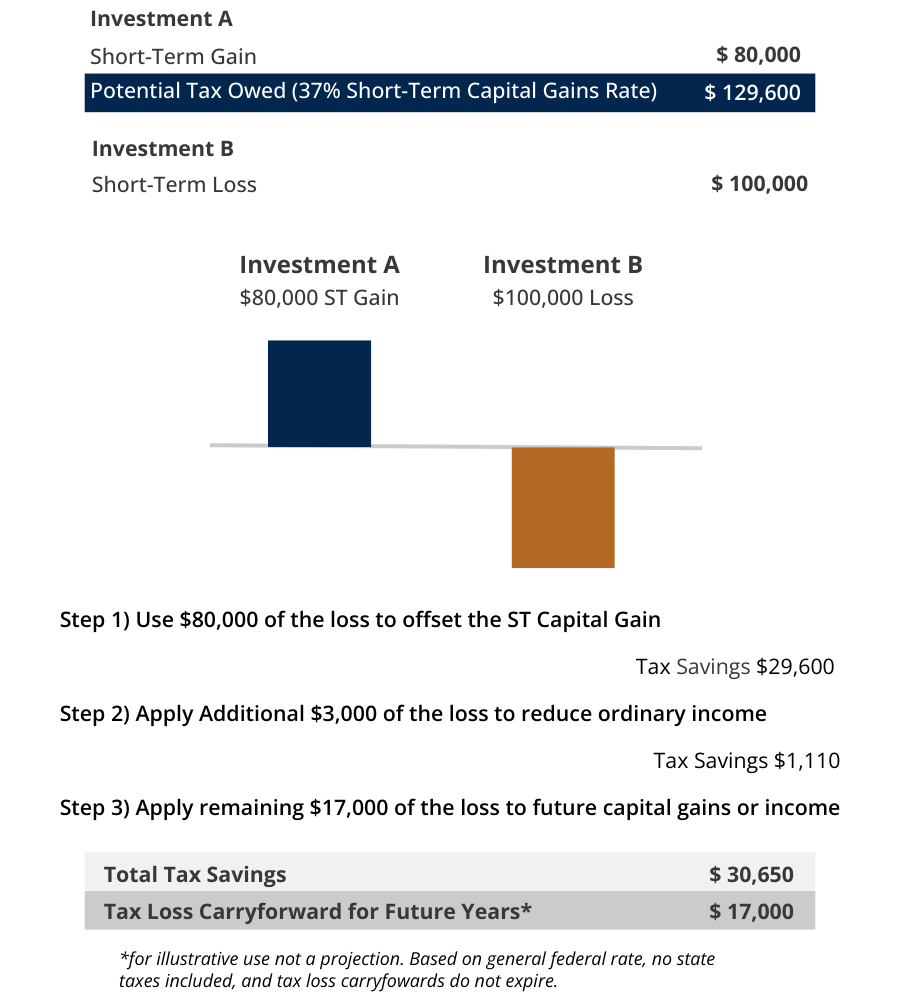

Tax Alpha Hypothetical Example:

Investment A incurs an $80,000 short-term gain, which generates a potential capital gains tax bill of $29,600. Investment B incurs a $100,000 loss. An investor might use $80,000 of that loss to offset the tax bill from Investment A. The investor could use another $3,000 of the loss to reduce ordinary income for that year and the remaining $17,000 to offset future gains.

Extension portfolios purchase additional select equities with the proceeds from short selling select equities. The most common form of these methods maintains 100% exposure to the market. These strategies can create more frequent and more durable tax alpha capture opportunities than traditional long-only portfolios because short positions generate losses as the market rises over time. When markets decline, there may be opportunities to generate tax losses in the long portfolio.

In general, a portfolio with both long and short positions creates more opportunities for investors to realize tax benefits.

Exchange funds allow clients to contribute concentrated stock positions into a fund with other investors’ concentrated stock holdings, receiving an interest in a more diversified basket of equities. Exchange funds usually require the investor to hold their position for seven years or face early redemption penalties and potential tax realization.

Individuals are most likely to face concentrated holdings after a business sale, IPO, equity compensation vesting, or when a long-held investment has significantly appreciated relative to the rest of their portfolio. An exchange fund can provide a path to diversification by allowing them to contribute their shares into a pooled vehicle in exchange for an interest in a broader basket of equities, typically without triggering an immediate taxable event.

351 ETF conversions have diversification requirements, which does not allow an investor to contribute a single appreciated stock. A client typically needs to own at least 10 stocks or ETFs to be eligible. In exchange for such contributions, clients receive a diversified ETF investment strategy that they can sell or hold at their discretion.

Clients should perform diligence on exchange funds and 351 ETF conversions to understand the associated management fees and investment strategies.

Charitable giving utilizes stock donations instead of cash. Investors can realize an immediate income tax deduction at full fair market value if deductions are itemized. They also avoid capital gains tax from having to sell the stock outright to generate cash.

Taking Control of Your Investment Returns

Caprock works closely with clients to develop customized strategies that best align with an individual’s liquidity needs, risk tolerance, and long-term goals.

Rather than a universal approach or model portfolio, our advisors take a holistic approach to a client’s balance sheet to help clients evaluate which methods support their desired after-tax returns goals.

Tax strategies are complicated and include a significant amount of nuances. Contact Caprock for a personalized assessment.

©Caprock. All rights reserved. The Caprock Group, LLC (“Caprock”) is an SEC Registered Investment Advisor. This communication is not an offer or solicitation with respect to the purchase or sale of any security and is for informational purposes only. Information contained herein has been derived from sources believed to be reliable, but Caprock makes no representations as to its accuracy or completeness. Investment in securities involves the risk of loss. Past performance is no guarantee of future returns. Registration with the SEC does not imply a certain level of skill or training. Caprock, its Employees, Affiliates and Advisers are not tax or legal professionals and do not provide such advice. Therefore, the discussions contained herein are for informational purposes only and should not be construed as a recommendation or endorsement of a strategy. Please consult with your tax or legal professional for further guidance and information. Caprock invests client capital through a variety of structures, including blended vehicles and direct investments.