The question is no longer whether international equities belong in a portfolio but what role they are expected to play. For years, sophisticated investors treated global diversification as a given. That logic made sense for a long time. It doesn’t anymore. After nearly a four-decade-long stretch of U.S. outperformance, global investments deserve a more rigorous review.

International stocks can still play an important role in a portfolio, but not simply because they offer geographic diversification. Global markets now move together more than they used to. In the past, some foreign markets held up better during volatile times. Today, stocks around the world often correlate to one another, so regional diversification doesn’t always offer the protection investors used to count on.

This raises an important question: What role should international investing play today, if any?

To evaluate that question well, it helps to separate headline diversification from portfolio usefulness: what has driven the gap between U.S. and international equity performance, what would need to change for that gap to narrow, and where international exposure may still earn its place?

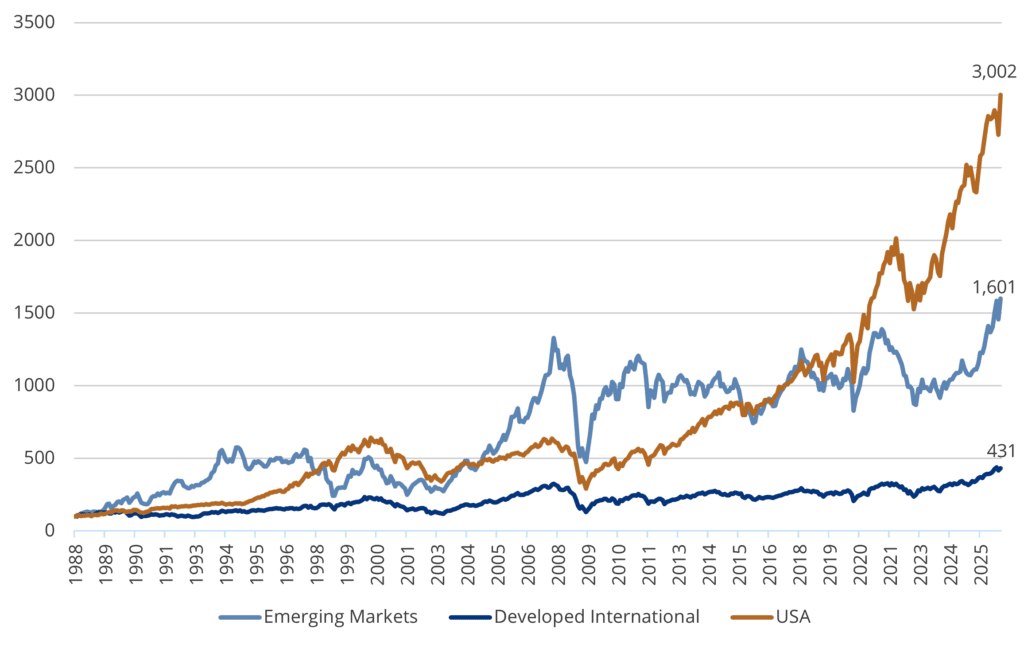

Cumulative Performance (indexed to 100)

Source for charts: LSEG Datastream

Emerging Markets have experienced intermittent periods of relative outperformance during strong global economic backdrops, justifying a strategic allocation at global equity benchmark weights.

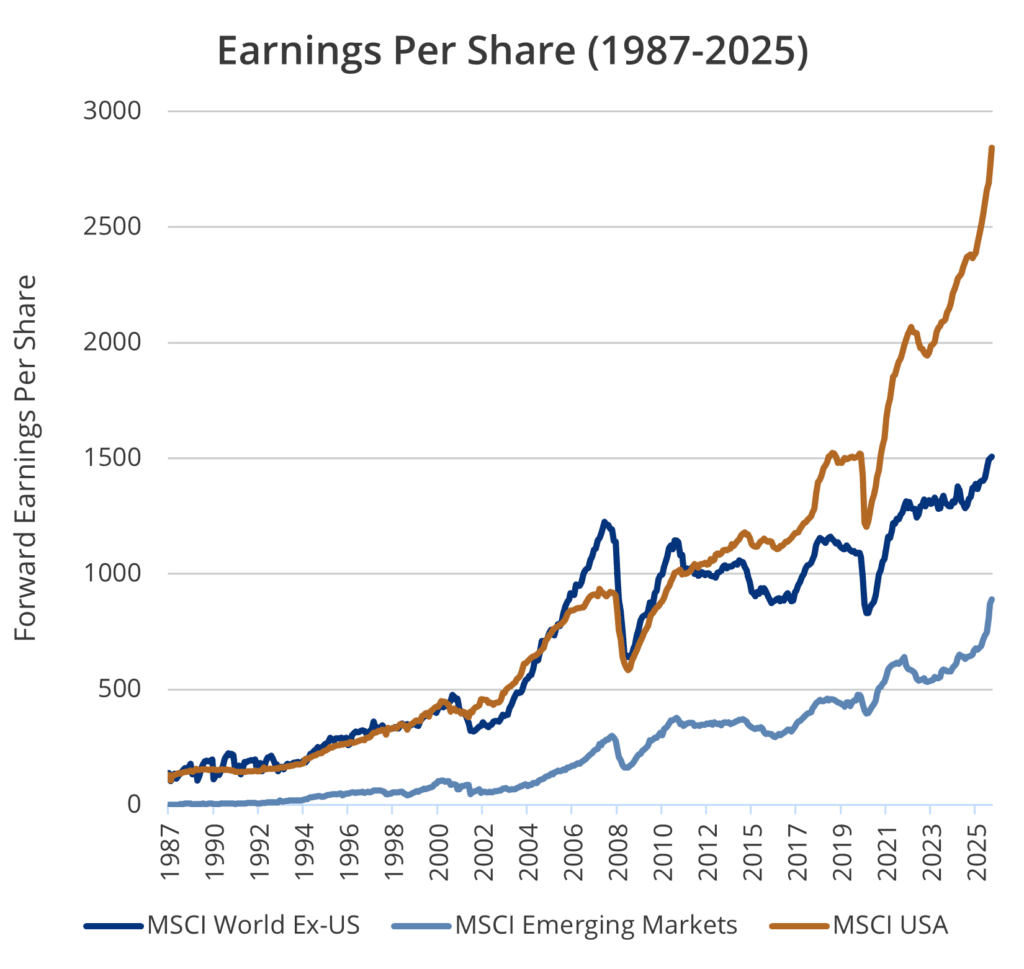

Why U.S. Stocks Have Outperformed International Equities

One reason U.S. equities have led for so long is that American companies have delivered stronger earnings growth than many of their global peers. Over time, that has mattered more than valuation narratives or short-term market rotations.

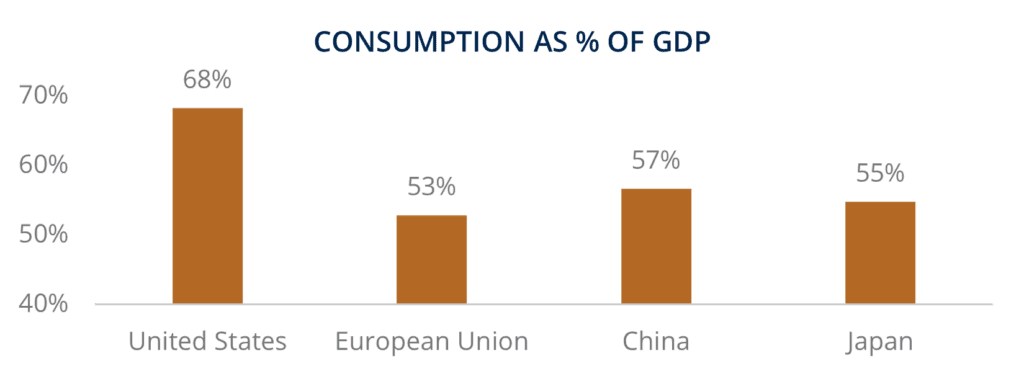

Part of the explanation is structural. The U.S. has a large consumer economy, deep capital markets, a strong innovation ecosystem and a corporate base with meaningful operating leverage. Consumer spending makes up a bigger part of the U.S. economy, roughly 68%, than in Europe or Japan, and it happens on a much larger scale. Relative to many developed markets, those conditions have supported more durable growth in revenues and profits.

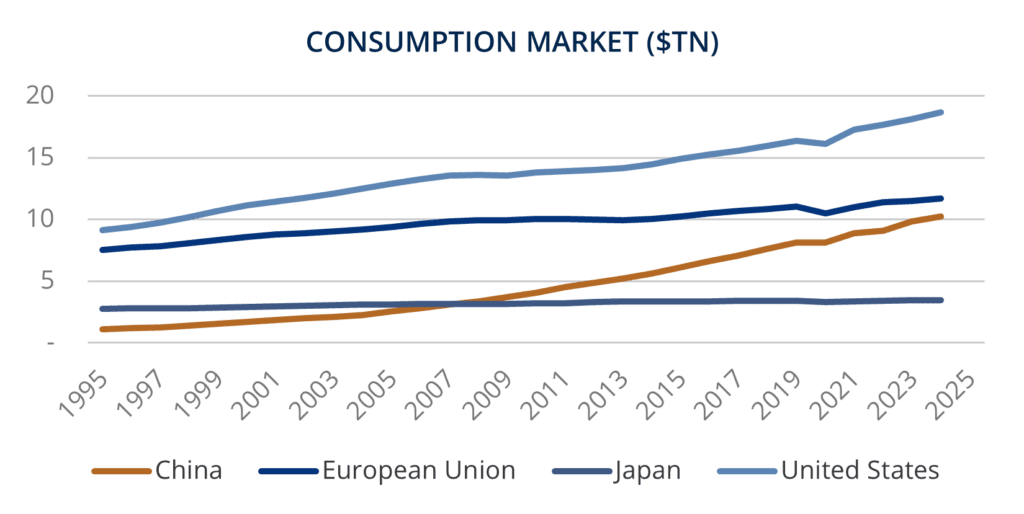

Advantages of Consumption-Based Economies

Consumption-based economies create a stable engine for growth, helping the economy to remain resilient during periods of uncertainty, and the U.S. is heavily oriented towards this type of growth.

The U.S. is the largest consumption market by a wide margin which offers unique advantages.

The robust consumer market in the U.S. has contributed to stable GDP growth alongside other factors

Source for charts: World Bank Global Consumption Database

That does not make the U.S. immune to drawdowns, valuation resets or cyclical weakness. It does suggest, however, that recent outperformance has not been purely accidental. In many cases, it has been supported by stronger underlying business fundamentals.

That is why the case for increasing international exposure cannot rest on mean reversion alone. A sustained shift in leadership would likely require a change in the underlying earnings picture, not simply the passage of time.

Why Lower Valuations Alone Do Not Make International Stocks Attractive

After decades of U.S. outperformance, international equities can look attractive simply because they trade at lower valuations. That observation is not wrong. Price alone, however, isn’t enough of a reason to buy a stock.

A discount only matters if it points to a better future than the market already expects. In some cases, lower valuations reflect overlooked opportunities. In others, they reflect weaker profitability, lower returns on capital or structural constraints that make faster earnings growth harder to sustain.

For international equities to close the gap in a durable way, the earnings picture would likely need to improve meaningfully. A stronger global economy could lift results across many regions and create periods of relative strength abroad, but that alone does not resolve the longer-term question.

International markets can lead for short periods, especially when global growth broadens, the dollar weakens or investor risk appetite improves. But for families allocating capital with a long horizon, the more important question is whether those conditions support a durable case for ownership rather than a temporary rotation.

Where International Exposure Still Adds Value

Coming back to our main question, if broad international exposure is less dependable as a general counterweight to U.S. stocks, the stronger case for what role it should play becomes more specific. The opportunity may lie in demographic change, rising household wealth, expanding consumer demand or industries that are developing on different timelines across regions.

Emerging markets illustrate that point. They can offer access to economic growth that is difficult to replicate through U.S. stocks alone, but that opportunity comes with wider outcomes and greater implementation complexity. For clients with long time horizons, sufficient liquidity and tolerance for volatility, that tradeoff may be worth underwriting. For others, it may not.

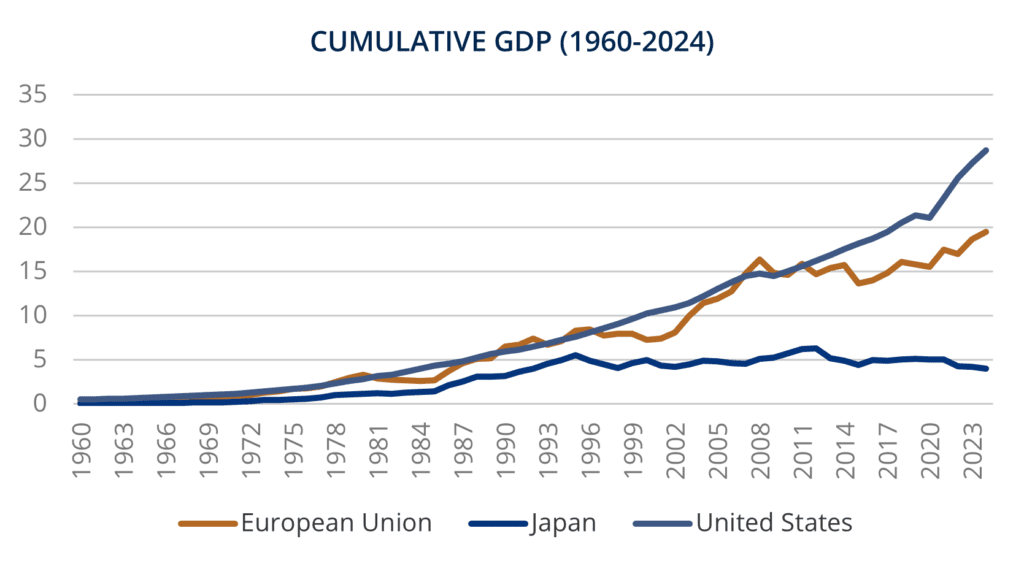

Source for charts: LSEG Datastream

The structural economic and financial market advantages of the U.S. have translated into a larger absolute value of earnings that has grown faster than the rest of the world.

Developed international markets require a different lens. A broad allocation may be less compelling when earnings growth remains weaker and leadership appears only in shorter bursts. Even so, individual companies, sectors or regions can still merit attention when the return drivers are clear and the opportunity is differentiated enough to justify the risk.

It is also important to start with what the portfolio already owns. Many large U.S. businesses generate substantial revenue overseas, which means domestic equity exposure may already provide meaningful participation in global growth. That does not eliminate the case for direct international investing, but it does raise the underwriting standard. Before adding more exposure, investors should understand how much global growth is already embedded in the portfolio.

Timing matters as well, but it is rarely the most reliable foundation for strategic allocation. International markets can benefit when global growth strengthens, currencies move in their favor or investor sentiment broadens beyond the U.S. Yet those windows are difficult to identify consistently, especially for portfolios built around long-term objectives rather than short-term trades.

At Caprock, this is where the analysis becomes more practical. As a multi-family office, we are less focused whether a family owns enough international stocks in the abstract, but whether that exposure adds something distinct once the full portfolio is taken into account—public and private holdings, liquidity needs, tax sensitivity and the ability to stay invested through periods of underperformance.

How High-Net-Worth Families Should Evaluate Global Equity Allocation

For families and their independent advisors, the next step is to evaluate international equities based on function, not just geography. The relevant question is not how much non-U.S. exposure a portfolio holds on paper, but what role that exposure is meant to play and whether it improves the portfolio in a way that is durable and useful.

That answer will vary by family. In some cases, the most compelling opportunity may be long-term exposure to emerging-market growth. In others, it may come through a narrower set of companies, sectors or regions in developed markets. Taxable investors may also weigh turnover, liquidity and implementation costs differently than institutions operating under a different set of constraints.

This is where broad labels can become misleading. Terms such as “international,” “developed markets,” and “emerging markets” describe where an investment is based but not whether it introduces a new source of return, offsets a risk the portfolio actually has or simply duplicates exposure already present elsewhere.

Caprock’s role is to make that distinction clear. In some portfolios, direct international exposure may earn its place. In others, the better answer may be a smaller allocation, a more targeted strategy or no change at all. The goal is not geographic completeness for its own sake, but a portfolio in which each allocation has a clear purpose.

For sophisticated investors, international equity exposure should be intentional, not inherited. The optimal allocation depends on what the portfolio already owns, what risks it still needs to absorb and what tradeoffs are worth making. For families with complex balance sheets, that is rarely a default setting. It is a portfolio design decision that a multi-family office can provide.

Learn more about diversified investment opportunities.

©Caprock. All rights reserved. The Caprock Group, LLC (“Caprock”) is an SEC Registered Investment Advisor. This communication is not an offer or solicitation with respect to the purchase or sale of any security and is for informational purposes only. Information contained herein has been derived from sources believed to be reliable, but Caprock makes no representations as to its accuracy or completeness. Investment in securities involves the risk of loss. Past performance is no guarantee of future returns. Registration with the SEC does not imply a certain level of skill or training. Caprock, its Employees, Affiliates and Advisers are not tax or legal professionals and do not provide such advice. Therefore, the discussions contained herein are for informational purposes only and should not be construed as a recommendation or endorsement of a strategy. Please consult with your tax or legal professional for further guidance and information. Caprock invests client capital through a variety of structures, including blended vehicles and direct investments.